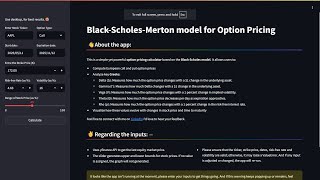

Media Summary: This video showcases my CS50P final project: a Option Pricing Black Sholes Merton BSM model in python Python Code: ... I look at using Newton's method to solve for the implied volatility of an

Black Scholes In Python Option Pricing Made Easy - Detailed Analysis & Overview

This video showcases my CS50P final project: a Option Pricing Black Sholes Merton BSM model in python Python Code: ... I look at using Newton's method to solve for the implied volatility of an What kind of content do you want to see? Answer this short survey to share what videos you like and what you want to see more ... Created by Sal Khan. Watch the next lesson: ... In this post, we focus on the implementation of the