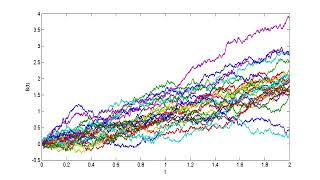

Media Summary: MC MOOC (Chapter 4.06): Wiener process. Statistical properties MC MOOC (Chapter 4.05): Simulation of a Wiener process MC MOOC (Chapter 4.09): Arithmetic Brownian motion. Statistical properties

Mc Mooc Chapter 4 06 Wiener Process Statistical Properties - Detailed Analysis & Overview

MC MOOC (Chapter 4.06): Wiener process. Statistical properties MC MOOC (Chapter 4.05): Simulation of a Wiener process MC MOOC (Chapter 4.09): Arithmetic Brownian motion. Statistical properties MC MOOC (Chapter 4.07): Wiener process. Time of first passage and distribution of maxima Understanding Black-Scholes (Part 2) This video is part of my series on the Black-Scholes model. I know that the theory is not ... MC MOOC (Chapter 3.08): The homogeneous Poisson process

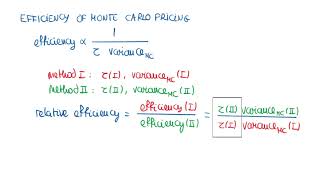

MC MOOC (Chapter 4.08): Arithmetic Brownian motion MC MOOC (Chapter 7.07): Efficiency of variance reduction methods in Monte Carlo pricing Quantitative finance can be a confusing area of study and the mix of math,